A Complete Guide to Tech Insurance for Modern Businesses

In a world that runs on code and data, tech insurance is a core part of your business's survival kit. Think of it as a specialized safety net, designed specifically for companies that build, sell, or depend on technology.

This kind of insurance covers the unique risks that come with digital operations, risks that your standard business policy probably won’t even touch. We’re talking about everything from a massive data breach to a critical software failure. It's the strategic shield that keeps you in business when your digital world gets messy.

Why Tech Insurance Is No Longer Optional

Let’s get real for a moment. Imagine a nasty bug in your flagship software costs a key client a fortune. Or a cyberattack freezes your entire operation, stopping revenue in its tracks. These aren't just scary stories; they're the real-world scenarios that make tech insurance so critical.

Traditional business policies were written for a physical world, covering things like a slip-and-fall in the lobby or a fire in the warehouse. But what about a server crash? Or a data breach that leaks thousands of customer records? A general liability policy is silent on these issues.

When a single line of bad code can spark a multi-million dollar lawsuit, sticking with old-school insurance is a gamble you can't afford to take. That's exactly where tech insurance fills the gap, offering protection built for the intangible, but incredibly valuable, assets that power your company.

The Modern Threat Landscape Demands Specialized Coverage

The digital battlefield is more complicated than ever. Threats are coming from all sides, and you need a defense strategy that's just as sophisticated.

Here’s a look at what you’re up against:

-

Sophisticated Cyberattacks: Ransomware, phishing, and denial-of-service (DoS) attacks aren’t just random; they’re targeted, clever, and designed to do maximum damage.

-

Software Performance Failures: Bugs, glitches, or a system that just doesn't play well with others can cause serious downtime and lead straight to angry clients and legal disputes.

-

Digital Supply Chain Vulnerabilities: Your security is only as strong as its weakest link. A vulnerability in a third-party tool or API can become an open door for attackers to walk right into your network.

-

Intellectual Property Theft: Your code, algorithms, and proprietary data are your secret sauce. Protecting them is non-negotiable if you want to stay ahead of the competition.

With cyber threats constantly on the rise, understanding standards like What is SOC 2 compliance offers a framework for managing these risks and highlights why specialized coverage is so essential.

Working with the right AI solutions partner can help you build the kind of resilient, secure systems that insurers want to see, which can strengthen your position. This is becoming more important as the insurtech market—where technology and insurance meet—is expected to grow by a staggering USD 114.39 billion by 2029. This boom proves that tech insurance isn't just a trend; it's the future of doing business safely.

Decoding Your Core Tech Insurance Coverage

Trying to get a handle on tech insurance can feel like learning a new language. You've got policies full of jargon, each one covering a very specific, and often confusing, set of risks. But for any company playing in the digital space, cutting through that noise is non-negotiable.

The best way to think about it is like building a specialized security team. You wouldn't hire a bodyguard to do a cryptographer's job, right? Same principle. You need a portfolio of policies, each designed to defend against a different kind of threat. Let's break down the four core players you need on your team.

Tech Errors & Omissions (E&O): The Professional Safety Net

Picture this: your company runs a critical SaaS platform for e-commerce clients. A bug in your latest software update brings their checkout systems to a screeching halt for an entire day. That’s thousands in lost revenue, and you can bet they’ll be looking to you to make it right.

This is exactly what Tech Errors & Omissions (E&O) insurance is for.

Think of E&O as malpractice insurance for the tech world. It’s there to protect your business when you're accused of negligence or your service fails to perform as promised. If your code, advice, or platform causes a client a direct financial loss, this policy kicks in to cover legal defense costs and potential settlements.

For any company whose product or service can directly mess with a client's bottom line, E&O is foundational. It’s your first line of defense against professional liability claims.

Cyber Liability Insurance: Your Digital Crisis Response Team

While E&O is all about your professional slip-ups, Cyber Liability insurance is your go-to for managing the fallout from digital threats—both external and internal. A data breach is one of the most common and devastating risks a business faces today. In fact, the average cost has now ballooned to $4.45 million.

This policy is designed to handle the absolute chaos and staggering expense of a security incident. It’s not just about the hack itself, but everything that comes after. Key protections usually include:

-

Breach Notification Costs: Paying to inform every affected customer, which is often required by law.

-

Credit Monitoring: Offering services to customers whose private information was exposed.

-

Public Relations: Hiring experts to manage your reputation and rebuild trust after a public incident.

-

Regulatory Fines: Covering penalties from government bodies for failing to protect data properly.

If you handle any kind of sensitive data – from simple email lists to credit card numbers – this coverage is an absolute must-have.

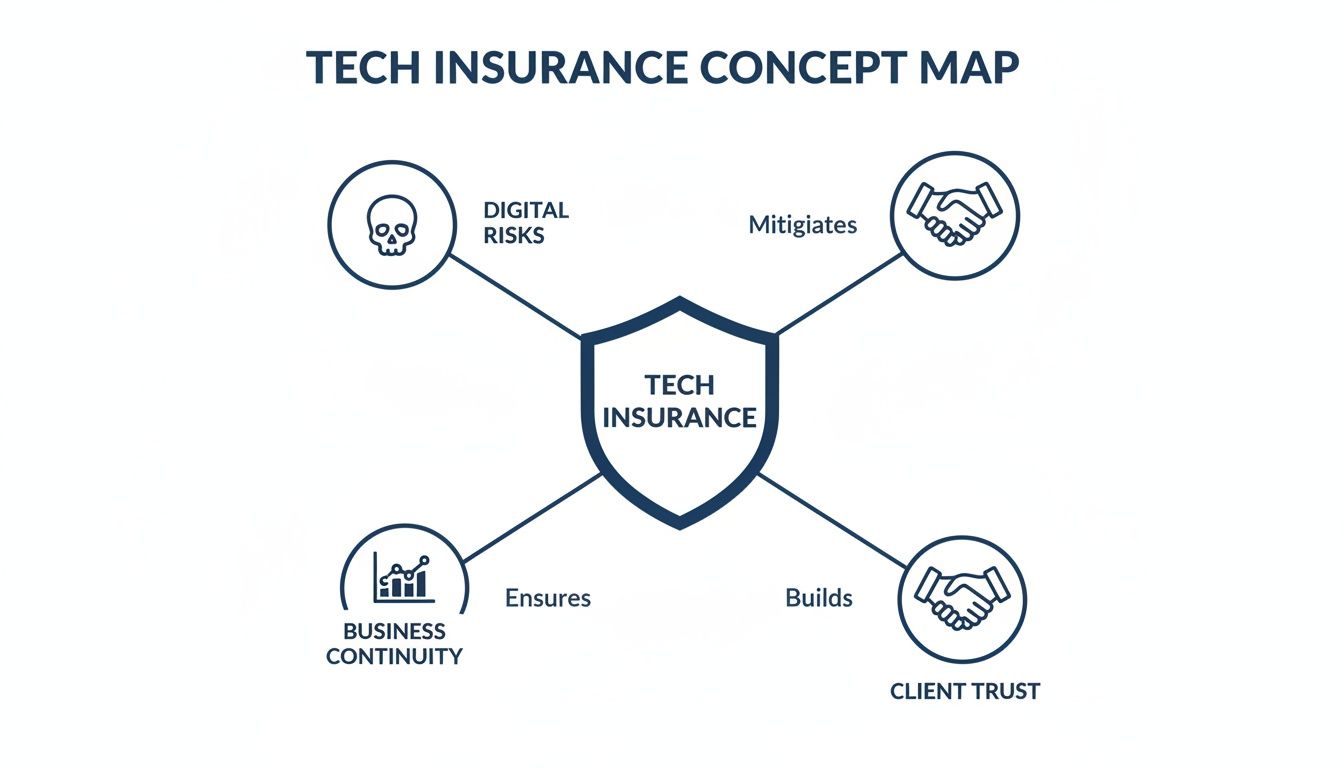

This concept map shows how tech insurance is more than just a line item in your budget; it’s a core strategy for managing risk, staying afloat during a crisis, and proving your reliability to clients.

As you can see, a solid insurance strategy is what allows a tech business to be resilient, not just reactive.

Key Tech Insurance Policies at a Glance

To make this even clearer, let's put these core coverages side-by-side. Each one plays a unique role in protecting your company from the different angles of digital risk.

| Coverage Type | What It Covers | Example Scenario |

|---|---|---|

| Tech Errors & Omissions (E&O) | Financial loss to a client due to your service failing, a bug in your software, or professional negligence. | Your project management software goes down for 48 hours, causing your client to miss a critical project deadline. |

| Cyber Liability | Costs from a data breach or security failure, including notification, credit monitoring, PR, and regulatory fines. | A hacker steals your customer database, and you have to notify 50,000 users and offer them identity protection. |

| First-Party Tech Loss | Direct financial losses to your own business after a cyberattack, such as data recovery and business interruption. | A ransomware attack locks your files, and you lose three days of revenue while your team works to restore systems. |

| Media Liability | Claims related to the content you publish, like copyright infringement, defamation (slander/libel), or invasion of privacy. | Your marketing team uses an image in a blog post without the proper license, and the photographer sues you. |

Understanding these distinctions is the first step toward building a truly comprehensive risk management plan that fits your specific business operations.

First-Party Tech Loss: Your Internal Recovery Fund

So, what happens when the attack hits your systems directly? A ransomware attack encrypts all your mission-critical data, and suddenly your entire operation grinds to a halt. The financial bleeding starts immediately, and every second of downtime costs you money.

First-Party Tech Loss coverage is designed to cover the costs you eat yourself. You can think of it as business interruption insurance built for the digital age. It helps you get back on your feet after your own network or data takes a hit, covering expenses like:

-

Data Restoration: The high cost of recovering, recreating, or restoring data that was corrupted or destroyed.

-

Ransom Payments: Funds to pay cybercriminals in a ransomware attack (though policy specifics can vary here).

-

Business Interruption: Compensation for the income you lost while your operations were down.

This policy is what ensures an attack on your own house doesn't turn into a complete financial catastrophe.

Media Liability: Protecting Your Digital Voice

In today's content-obsessed world, every blog post, social media update, and ad you publish is a potential landmine. A harmless-looking marketing image could spark a copyright infringement lawsuit. A competitor could claim your ad copy defamed them.

Media Liability insurance is your shield against these exact risks. It protects you from claims that pop up because of the content you create and share, including:

-

Defamation (both libel and slander)

-

Copyright or trademark infringement

-

Invasion of privacy

For any company with a website, a blog, or a social media account – which is pretty much everyone – this coverage is a critical backstop for all marketing and communication efforts. As we explored in our guide to AI in the insurance industry, underwriters are getting smarter about pricing these complex risks, making well-defined coverage more essential than ever.

The Top Digital Risks Modern Tech Companies Face

To really get a feel for why tech insurance matters, you have to look past the industry jargon and into the real-world nightmares that keep CTOs and founders up at night. These aren't just things you read about in the news; they are tangible, expensive, and increasingly common events that can absolutely wreck a business without the right safety net.

For any tech company today, your digital footprint is your greatest strength and your biggest weakness. A single vulnerability can set off a chain reaction, leading to staggering financial losses and a reputation that’s hard, if not impossible, to repair. Let's dig into the specific risks that make this kind of insurance non-negotiable.

The Ever-Present Threat of Cyberattacks

Cyberattacks are the most obvious and often most destructive risk out there. But we've moved way beyond simple viruses. Today's threats are sophisticated, targeted, and built to cause maximum chaos.

-

Crippling Ransomware: Picture this: your entire codebase, development servers, and customer database are locked down by encryption. The attackers want a seven-figure payment to give you the key. This isn't just a data breach; your entire operation grinds to a halt. Every second of downtime means lost sales, shattered customer trust, and a frantic, all-hands-on-deck recovery effort.

-

Intellectual Property (IP) Theft: Your proprietary code, unique algorithms, and business plans are the lifeblood of your company. A breach that specifically targets and steals this IP can effectively hand your competitive edge to a rival. It’s a devastating blow that can take years to recover from, if ever.

-

Business Email Compromise (BEC): These aren't your average spam emails. BEC attacks are clever phishing schemes that trick key employees into wiring funds or giving up sensitive credentials. One convincing-looking email from a spoofed executive account can result in hundreds of thousands of dollars being sent straight to a criminal's bank account.

Software Performance and Liability Failures

Not all threats are external. Sometimes, the biggest dangers are baked right into your own products and services. A bug in your code or an unexpected system outage can be just as costly as a malicious hack.

When your technology is the product, any failure to perform as promised becomes a direct liability. This is where lawsuits for negligence or breach of contract crop up, turning a technical glitch into a legal and financial nightmare.

Think about what happens if your API goes down, causing a major outage for a key enterprise client who depends on your service for their own operations. The business interruption claim they could file against you could be massive. The first and best defense is always proactive risk mitigation through secure custom software development, but insurance is the backstop for when things inevitably go wrong. Pinpointing these potential failure points is central to smart planning, a topic we explored in our guide on how to approach software project risk management.

The Growing Danger of Digital Supply Chain Attacks

Your business doesn't exist in a bubble. You rely on a complex network of third-party tools, APIs, and cloud services to get work done. This interconnectedness creates a huge, and often ignored, attack surface: the digital supply chain.

A vulnerability in a third-party software library you use or a security breach at one of your cloud providers can become a backdoor right into your own systems. Your internal security could be flawless, but if a trusted partner is compromised, you inherit all their risk. This makes vetting your vendors’ security just as critical as managing your own.

It's no surprise the cyber insurance market has tripled in size over the last five years, trying to keep pace with this explosion in risk. Still, global economic losses from events like these have left a staggering 60% protection gap. We're talking about US$944 billion in insured losses against US$2,349 billion in total economic losses. Insurers are now laser-focused on ransomware and supply chain weak points, creating an urgent need for better systems to close that gap. You can discover more insights on the global insurance outlook from EY.com.

How AI Is Reshaping the Insurance Landscape

For decades, the insurance industry ran on paper, historical data tables, and a whole lot of educated guesswork. That era is over. The engine driving this change is artificial intelligence, and it’s fundamentally shifting how insurance works. Insurers are moving from reacting to events to actively predicting them, an evolution that touches everything from policy pricing to claim payouts.

This isn't just an internal shift for insurers; it's a massive opportunity for your business. The same AI that's making the insurance world smarter can also make your company a much better, more attractive risk. When you build AI into your own operations, you're sending a clear signal to underwriters that you're serious about managing risk. This is more than just a tech upgrade. It's a strategic play to lock in better coverage and better terms.

Smarter Underwriting Through AI

The old way of underwriting was a bit like driving while looking in the rearview mirror. Insurers analyzed past data to set premiums for the future, lumping businesses into broad, generic categories. AI completely flips that model on its head, enabling dynamic risk modeling that assesses your specific situation in real time.

Today, machine learning algorithms can sift through thousands of data points at once, everything from your company's cybersecurity posture to the specific way your team develops software. This creates a highly customized risk profile for your business, pulling you out of the generic industry bucket. As we’ve covered in our deep dive on AI in the insurance industry, this move toward personalization leads to far more accurate and fair pricing.

The Impact of AI on Claims Processing

Let’s be honest: the claims process has always been a major headache, for both insurers and their customers. It was often a slow, manual crawl through paperwork and reviews. AI is injecting much-needed speed and intelligence into every step.

By taking over routine tasks and flagging only the truly complex cases for a human expert, AI-driven systems can push claims through in a fraction of the time. For businesses, this means getting critical funds faster when you need them most, helping you get back on your feet after an incident.

Here’s where you can see the difference:

-

Fraud Detection: AI algorithms are incredible at spotting suspicious patterns in claims data that a person might easily miss. This helps cut down on fraudulent payouts and keeps premiums more stable for everyone.

-

Automated Assessment: For more straightforward claims, an AI can analyze the documents, check them against the policy details, and approve the payment without any human needing to touch it.

-

Customer Support: AI-powered chatbots now act as the first line of support, answering initial questions 24/7 and walking policyholders through the first steps of making a claim. In fact, 42% of P&C insurers are already piloting AI-assisted customer support, showing just how fast this is becoming the norm.

How Your Business Can Become More Insurable with AI

Here’s the most important takeaway: you can directly improve your company's risk profile by adopting the same kinds of technologies that insurers are using. When an underwriter sees you’re using AI to get ahead of risks, you immediately become a much more appealing client.

This is where investing in expert AI development services pays dividends. By building systems that prove your commitment to security and operational discipline, you’re giving underwriters concrete data to justify better terms. For example, an AI-driven cybersecurity platform that predicts and stops threats before they happen is one of the strongest signals you can send.

Think about these practical applications:

-

Predictive Maintenance: If you manage physical tech infrastructure, AI can predict hardware failures before they happen, preventing the kind of costly downtime that leads to business interruption claims. Read more here.

-

Enhanced Cybersecurity: Sophisticated AI systems can monitor network traffic for unusual activity, identifying potential attacks in real time and automatically isolating threats.

-

Code Quality Analysis: You can use AI tools to scan your codebase for vulnerabilities during the development cycle, squashing bugs that could later turn into expensive E&O claims.

In the end, it all comes down to showing that you’re proactive, not reactive. Bringing AI for your business isn't just about efficiency; it's about building a fundamentally more resilient and insurable company. When you can show underwriters that you have smart systems in place to prevent losses, you give them the data-backed confidence they need to offer you the best tech insurance possible.

Strengthening Your Insurability Through Digital Transformation

When it comes to tech insurance, your risk profile isn’t set in stone. It’s a living measure of your company’s tech maturity and operational discipline. Insurers today dig much deeper than your revenue or industry; they’re getting under the hood to inspect your digital infrastructure, security protocols, and even your development practices. The secret to getting better premiums is about becoming a fundamentally safer bet.

This is where a real digital transformation comes in. It’s not just about buying new tools. It's about strategically using technology to build a more resilient, more defensible business. This journey can turn your company from just another applicant into a preferred partner in the eyes of an underwriter.

From Vulnerable Legacy Systems to Modern Resilience

Nothing screams "risk" to an insurer quite like legacy systems. These old platforms are often full of unpatched holes, are a nightmare to secure, and cost a fortune to maintain, making them a juicy target for cybercriminals. Moving off them is one of the clearest signals you can send about your commitment to security.

A modern tech stack shows underwriters that you've got your act together. Specifically, it proves you have:

-

Robust Security Controls: Modern platforms are designed for today's threats, making it far simpler to implement essentials like multi-factor authentication (MFA) and end-to-end encryption.

-

Active Support and Patching: Unlike that old software gathering dust, modern systems get regular security updates to stay ahead of new threats.

-

Greater Scalability and Reliability: A cloud-native setup and resilient architecture drastically cut the risk of expensive downtime and business interruption claims.

Putting money into modern insurance software solutions doesn't just make your own operations smoother; it serves as concrete evidence of your diligence when you’re filling out that insurance application. We've seen it firsthand in our client cases. This kind of tech commitment can directly translate into better policy terms.

Embedding a Security-First Development Lifecycle

How you build your products is just as critical as what they do. Adopting a "security-first" culture, you might know it as DevSecOps, means weaving security checks into every stage of the development process, not just slapping them on at the end like an afterthought. This approach drastically cuts the chances of bugs and vulnerabilities ever seeing the light of day.

Shifting to a security-first culture means moving from a reactive "find and fix" scramble to a proactive "prevent and protect" strategy. It tells an insurer that you're working hard to stop a Tech E&O claim from ever happening.

Beyond just good coding hygiene, developing an actionable disaster recovery plan for IT is another way to show you’re serious about managing risk from all angles—something underwriters absolutely love to see. Our guide on digital transformation best practices offers more on building this kind of tough, resilient framework.

The Data-Driven Underwriting Landscape

The insurance world is going through its own tech revolution. IT spending in the sector is on track to hit $291 billion next year, with much of that cash flowing into AI-powered tools for risk assessment and claims processing. What this means for you is that underwriters are using smarter, more sophisticated methods to size up your company.

Your own investment in modern technology feeds these AI models the exact kind of positive data they’re designed to find. When you can show off a strong security posture, automated compliance, and a resilient infrastructure, you're speaking the language of modern underwriting. This data-backed proof that you're a low-risk operation is your ticket to getting the best possible tech insurance coverage at a price that makes sense.

Your Practical Checklist for Buying Tech Insurance

Buying tech insurance isn't like picking a plan off a shelf; it's a strategic move that demands a serious look at your company's specific vulnerabilities. Think of this checklist as your game plan for getting coverage that actually works when you need it most.

Step 1: Map Your Real-World Risks

Before you even think about talking to a broker, you need to look in the mirror. A candid internal audit is the bedrock of a good insurance strategy. It’s how you figure out what you’re really trying to protect.

-

Follow the data: Where does all your sensitive information live? Pinpoint everything from customer PII and financial data to your proprietary source code. Know where it is, how it moves, and who can access it.

-

Identify your linchpins: What systems, software, or third-party APIs would bring your business to a halt if they went down? What's the real-world impact of an outage?

-

Get honest about your defenses: Where are the cracks in your armor? Make a list of your current security controls—everything from multi-factor authentication and encryption to how you train your team on phishing. No sugarcoating.

Step 2: Get Your Paperwork in Order

Underwriters don't just take your word for it—they base their decisions on hard evidence. Showing up with organized, comprehensive documentation signals that you're a serious, low-risk partner, which can directly impact your premiums.

A well-documented security and response strategy is your most persuasive tool in negotiations. It tells insurers you are a proactive partner, not a reactive liability.

Pull these documents together before you start shopping:

-

Incident Response Plan: This should be a detailed, step-by-step playbook for what your team will do the moment a breach is detected.

-

Security Protocol Summary: A clear overview of your cybersecurity measures, including firewall setups, encryption standards, and how often you run vulnerability scans.

-

Key Vendor Agreements: Dig into the SLAs and liability clauses for all your critical third-party services. You need to know where their responsibility ends and yours begins.

Step 3: Vet the Policy and the Broker

In the tech world, the details matter—and that’s especially true for insurance policies. The fine print can be the difference between a paid claim and a massive financial hit.

First, find a broker who lives and breathes technology risks. A generalist won't cut it. You need an expert who understands the nuances between different policies and can fight for the terms you need. When you're looking at quotes, zoom in on the limits, sub-limits, and exclusions. That’s where the nasty surprises hide.

Finally, make sure your policy has room to grow with your business. A static policy is useless for a scaling tech company. By preparing diligently and partnering with a true expert, you'll secure a tech insurance policy that's more than just a piece of paper—it's a real safeguard for your future. And as you scale, having a reliable AI solutions partner can help you continuously upgrade the systems that keep you insurable.

Frequently Asked Questions About Tech Insurance

It's natural to have questions when you're wading into the world of tech insurance. Let's cut through the noise and get straight to the answers you need to make smart, confident decisions for your business.

How is Tech E&O different from general liability insurance?

Think of it in terms of worlds: the physical versus the digital. A General Liability policy is built for the physical world—it covers things like a client slipping in your office (bodily injury) or accidentally damaging their server rack during an on-site visit (property damage).

Tech Errors & Omissions (E&O) insurance, however, lives squarely in the digital realm. It’s designed to cover the financial fallout your clients experience because of a mistake in your code, a service failure, or bad advice. If your SaaS platform goes down and causes a customer to lose thousands in sales, that’s a job for Tech E&O.

Will my policy cover a breach caused by an employee mistake?

Most of the time, yes. A solid Cyber Liability policy is built to respond to data breaches regardless of their origin, and that absolutely includes human error. After all, an employee accidentally clicking a phishing link is one of the most common ways breaches happen.

But there's a catch. Your insurer will want to see that you've done your part. They'll expect you to have basic security protocols and employee training programs in place. Being able to show you've taken reasonable precautions is crucial for getting your claim paid without a hitch.

What are the best ways to lower our premiums?

Insurers love to see proactive risk management—and they reward it with better pricing. The most direct way to lower your tech insurance premiums is to prove you have a strong, buttoned-up security posture.

Simple things make a huge difference. Implement multi-factor authentication (MFA) everywhere you can, run regular vulnerability scans on your systems, and have a clear, documented incident response plan ready to go. As we've discussed, working with a specialist in custom software development to build modern, secure applications from the ground up sends one of the most powerful messages to an underwriter.

Does tech insurance cover failures from third-party APIs?

This is a big one, and the answer is "it depends." Your standard policy might not automatically cover financial losses that stem from a third-party service you depend on.

This is precisely why you need to ask about contingent business interruption coverage. It’s an extension to your Cyber Liability policy designed for this exact scenario—protecting you when a critical vendor in your digital supply chain has an outage that brings your own operations to a halt.

Ready to build the resilient, secure, and AI-driven systems that modern insurers value? Bridge Global provides the expertise to strengthen your insurability and drive your business forward. Explore our AI-powered solutions today.

About Preethi Saro Philip

Preethi Saro Philip is a Post Graduate Research Degree holder in Economics with more than 10 years of experience in writing, editing, research and teaching. She has an intense passion for content crafting and calls herself a ‘wordsmith’. She enjoys writing on wide-ranging topics including business, technology, health & lifestyle, education, environment etc.

View all posts by Preethi Saro Philip →